The energy storage landscape is pulsating with a singular, potent rhythm. From corporate boardrooms to academic laboratories, the drumbeat for the solid-state battery grows louder and more synchronized. I observe a unique moment of convergence: a flurry of announcements on research milestones, aggressive capacity planning, and bold commercialization timelines, all underscored by significant theoretical breakthroughs. This triad—technology, manufacturing, and market readiness—is resonating at an unprecedented frequency, signaling that the long-anticipated solid-state battery is entering its final sprint. The core question on everyone’s mind is no longer “if” but “when” this technology will transition from controlled lab environments to mass production and finally “get on the vehicle.”

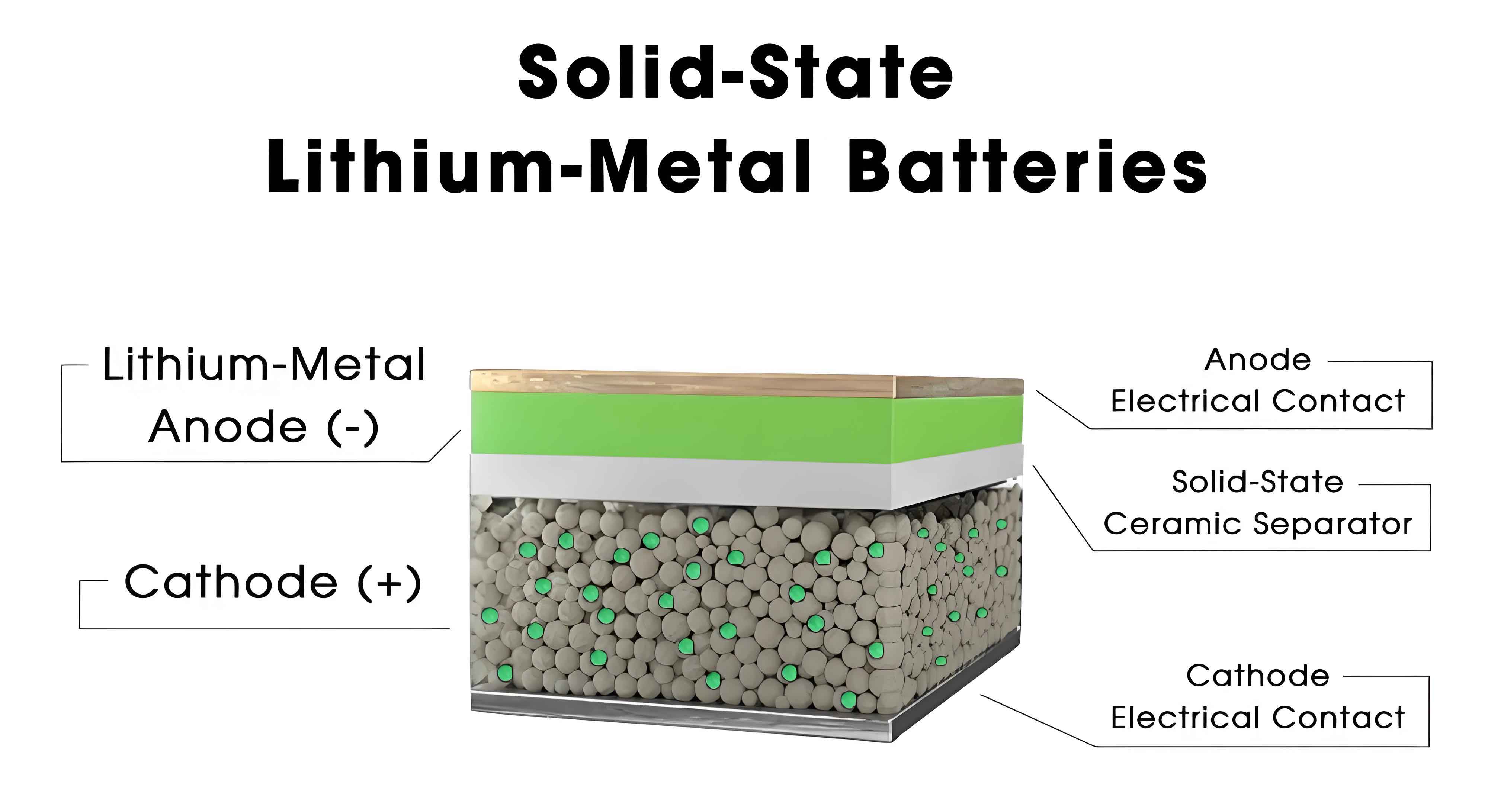

Fundamentally, a solid-state battery replaces the flammable liquid electrolyte found in conventional lithium-ion cells with a solid electrolyte. This single substitution is transformative, promising to tackle the two most persistent demons of electric mobility: range anxiety and safety risks. By enabling the use of high-capacity lithium metal anodes and offering superior thermal stability, the solid-state battery is often hailed as the “ultimate solution” for next-generation power batteries. However, for years, this promise remained confined to research papers, held back by intricate material science challenges, prohibitive costs, immature supply chains, and unclear commercialization pathways.

Recently, this static picture has dramatically shifted. The pace of progress has accelerated remarkably, compressing timelines that were once projected for the next decade. I see automotive OEMs and battery cell manufacturers not just hinting at future possibilities, but publicly charting specific roads to production. Concurrently, foundational research is solving critical bottlenecks that plagued the technology. This multi-front advance creates a powerful feedback loop: theoretical progress de-risks corporate investment, which in turn funds larger-scale development and pilot lines, pulling the technology closer to market viability.

The Tripartite Resonance: Theory, Capacity, and Commerce

The current excitement is not built on a single data point but on a web of interdependent advancements across the entire value chain.

1. Theoretical and Material Science Breakthroughs

The core challenges of the solid-state battery are deeply scientific. Key issues include low ionic conductivity of solid electrolytes, high interfacial impedance between the solid components, and the growth of lithium dendrites that can short-circuit the cell. Recent research is making meaningful inroads.

For instance, a significant breakthrough involves novel interfacial engineering techniques. One promising approach uses anion regulation strategies to modify the solid electrolyte interface (SEI) at the lithium metal anode. This creates a more stable and ionically conductive interphase, allowing for better contact and lower resistance. The charge transfer resistance at this critical interface can be modeled as part of the total cell impedance:

$$

R_{total} = R_{bulk} + R_{ct} + R_{sei}

$$

where $R_{bulk}$ is the bulk resistance of the electrolyte, $R_{ct}$ is the charge transfer resistance at the electrode/electrolyte interface, and $R_{sei}$ is the resistance of the interphase layer. Advanced interfacial engineering aims to minimize $R_{ct}$ and stabilize $R_{sei}$, which is crucial for achieving high current densities and long cycle life.

Another area of progress is in electrolyte itself. Researchers are developing new classes of solid electrolytes—sulfide-based, oxide-based, and polymer-based—each with trade-offs. Sulfides offer high ionic conductivity but stability issues, while oxides are stable but often require high sintering temperatures. The quest is for a material that balances conductivity, electrochemical stability, mechanical properties, and cost. The ionic conductivity $\sigma$ is a key metric, following an Arrhenius-type relationship with temperature:

$$

\sigma = A \exp\left(-\frac{E_a}{k_B T}\right)

$$

where $E_a$ is the activation energy for ion hopping, $k_B$ is Boltzmann’s constant, and $T$ is temperature. Lowering $E_a$ is a primary goal for enabling room-temperature performance.

| Electrolyte Type | Exemplar Material | Ionic Conductivity (S/cm, RT) | Key Advantage | Key Challenge |

|---|---|---|---|---|

| Sulfide | Li$_{10}$GeP$_2$S$_{12}$ (LGPS) | ~10$^{-2}$ | Very High Conductivity | Air Sensitivity, Cost |

| Oxide | Li$_{7}$La$_3$Zr$_2$O$_{12}$ (LLZO) | ~10$^{-4}$ to 10$^{-3}$ | Excellent Stability | Rigidity, Interface Issues |

| Polymer | PEO-LiTFSI | ~10$^{-5}$ to 10$^{-4}$ | Flexibility, Processability | Low RT Conductivity |

2. Capacity and Manufacturing Announcements

Theoretical promise is being translated into tangible industrial activity. The landscape is no longer dominated by pure-play startups; established battery giants and automotive leaders are now driving the agenda. I am tracking announcements that move beyond prototype cells to discussions of pilot lines, GWh-scale factory plans, and supply chain construction. This shift signifies a belief that core technical hurdles are being overcome, justifying capital expenditure on pre-production and production-scale infrastructure. The focus is on scaling the synthesis of sensitive solid electrolytes, developing novel cell assembly processes that maintain perfect interfacial contact, and integrating lithium metal anode handling—all in a cost-effective manner.

3. Commercialization Timelines and Vehicle Integration

This is where the resonance becomes most audible to the public. Major automakers from Asia, Europe, and North America are embedding solid-state battery technology into their product roadmaps. The proclaimed timelines for initial limited production or flagship model launch have clustered around the 2027-2028 window, with some aiming even sooner. These are not vague aspirations but are increasingly backed by partnerships with specialized battery firms, public road testing of validation vehicles, and specific energy density targets. The projected performance metrics are compelling, directly addressing consumer desires: energy densities exceeding 400 Wh/kg and even approaching 600 Wh/kg, which potentially doubles the range of today’s best electric vehicles (EVs) on a single charge. We can express the potential range increase simply as:

$$

\text{Range}_{SSB} \approx \text{Range}_{LIB} \times \frac{\text{Energy Density}_{SSB}}{\text{Energy Density}_{LIB}}

$$

If a current EV with a 350 Wh/kg battery achieves 500 km, a solid-state battery at 500 Wh/kg could theoretically achieve:

$$

\text{Range}_{SSB} \approx 500 \text{ km} \times \frac{500}{350} \approx 714 \text{ km}

$$

This simplistic calculation ignores packaging efficiency gains and other factors, but illustrates the transformative potential.

Quantifying the Leap: Performance and Safety Equations

The superiority of the solid-state battery can be framed through key performance indicators (KPIs). Let’s define them mathematically.

Gravimetric Energy Density ($E_g$): This is the most discussed metric.

$$

E_g = \frac{\text{Usable Energy (Wh)}}{\text{Battery Mass (kg)}}

$$

For a solid-state battery with a lithium metal anode, the theoretical maximum is significantly higher than for graphite-anode Li-ion. The practical target for first-generation solid-state battery cells is >400 Wh/kg, with a path to >500 Wh/kg.

Volumetric Energy Density ($E_v$): Also critical for vehicle design.

$$

E_v = \frac{\text{Usable Energy (Wh)}}{\text{Battery Volume (L)}}

$$

The removal of bulky liquid electrolyte and inactive components can improve $E_v$.

Safety Function ($S$): A qualitative but paramount advantage. We can model the risk of thermal runaway as a function of electrolyte stability and operating temperature.

$$

\text{Risk of Thermal Runaway} \propto \int_{T_{op}}^{T_{ignition}} \frac{1}{\Delta H_{decomp}} \cdot f(\text{electrolyte volatility}) \, dT

$$

Where $T_{op}$ is operating temperature, $T_{ignition}$ is ignition temperature, and $\Delta H_{decomp}$ is the heat of decomposition. The solid electrolyte’s non-volatility and high thermal stability increase $T_{ignition}$ and alter the function $f$, drastically reducing the integral’s value compared to liquid electrolytes.

| Parameter | Current Liquid Li-ion | Target for Solid-State Battery | Impact |

|---|---|---|---|

| Gravimetric Energy Density | ~250-300 Wh/kg (cell) | >400 Wh/kg (cell) | +60% range or reduced pack weight |

| Cycle Life (80% retention) | 1000-2000 cycles | >1000 cycles (initial target) | Comparable longevity for EVs |

| Charge Rate (Fast-charge) | 1-3C typical | Potential for >4C | Faster charging possible |

| Operating Temperature Range | -20°C to 60°C | Broader range possible | Improved performance in extreme climates |

| Thermal Runaway Risk | Present, requires management | Significantly Reduced | Eliminates major safety hazard, simplifies BMS and cooling |

The Remaining Hurdles: A Reality Check

Despite the palpable momentum, a measured perspective is essential. The path to ubiquitous solid-state battery “vehicles” is still paved with formidable challenges. Industry leaders rightly point out that many announced products are intermediate steps, often “semi-solid” batteries that retain a small amount of liquid or gel electrolyte to mitigate interface issues. A true, all-solid solid-state battery with lithium metal anode faces several steep barriers:

1. Cost and Supply Chain: The materials for solid electrolytes (e.g., germanium, lanthanum, tantalum) can be expensive or geopolitically sensitive. Manufacturing processes are new, requiring capital-intensive equipment and a learning curve to achieve yield. The cost per kilowatt-hour ($/kWh) for a solid-state battery is currently orders of magnitude higher than for liquid Li-ion. The cost equation must converge:

$$

C_{SSB} = C_{mat} + C_{proc} + C_{ovh}

$$

Where $C_{mat}$ is material cost, $C_{proc}$ is processing cost, and $C_{ovh}$ is overhead. Scaling production and discovering cheaper, abundant materials are needed to drive $C_{SSB}$ down to competitive levels, a process estimated by some to take a minimum of 3-5 years for a mature supply chain to develop.

2. Manufacturing Scalability: The delicate solid-solid interfaces require flawless, consistent fabrication. Processes like thin-film deposition, hot pressing, or aerosol deposition must be adapted for speed and scale while maintaining nanoscale precision. Any defect can lead to high resistance or failure.

3. Long-Term Reliability: While single cells show promising cycle life in labs, the performance of a full battery pack over 10+ years in diverse real-world conditions (vibration, temperature cycles, repeated fast charging) remains to be proven. The mechanical stress on solid interfaces during cycling is a critical unknown.

When Will We Truly See Mass “Adoption”?

Synthesizing the signals, I foresee a phased rollout rather than a sudden big bang.

Phase 1 (Now – ~2026): Limited Commercialization. The first “solid-state” batteries to market will likely be semi-solid variants, offering incremental improvements in energy density and safety. They may debut in premium vehicles, specialized applications (e.g., aerospace, luxury EVs), or as small-capacity cells in consumer electronics. These will serve as crucial learning platforms.

Phase 2 (~2027 – 2030): Niche Market Penetration. As several automakers hit their stated timelines, we will see the first production vehicles equipped with what they label as all-solid-state batteries. These will be low-volume, high-price tag models—flagships designed to showcase technological leadership. Energy densities of 400-500 Wh/kg at the cell level will be demonstrated. The focus will be on validating reliability and driving down costs through initial scale.

Phase 3 (Post-2030): Mainstream Expansion. This is the inflection point for true mass-market impact. By this time, manufacturing processes will have matured, supply chains will be established, and the total cost of ownership for a solid-state battery EV is expected to become competitive with advanced liquid Li-ion. Widespread adoption across multiple vehicle segments will then commence, fundamentally altering the performance benchmarks for electric vehicles.

The capital markets have already begun pricing in this future. The valuation surge in companies associated with solid-state battery technology reflects a bet on this timeline accelerating. However, some seasoned analysts maintain a more conservative view, awaiting “flagship events” like sustained, large-volume orders or the groundbreaking of dedicated “gigafactories” for all-solid-state cells before declaring the technology mainstream.

Conclusion: An Inevitable, Yet Complex, Transition

The solid-state battery is undeniably in its sprint phase. The simultaneous advances in foundational science, industrial capacity building, and concrete product planning create a powerful, self-reinforcing cycle of progress. The question has evolved from feasibility to one of timing and execution. While challenges around cost, scalable manufacturing, and long-term durability are real and significant, the collective force of global R&D and industrial might is now focused on solving them. The 1000-km range EV is not a mere fantasy but a probable outcome of this technology trajectory. The journey from lab to road is complex, but the destination—a safer, longer-range, and fundamentally better energy storage paradigm—is coming clearly into view. The race is on, and the finish line, though not immediately around the corner, is finally within the industry’s strategic horizon.