As an observer of global energy transitions, I find Bangladesh’s journey particularly compelling. The nation stands as one of the world’s fastest-growing economies, yet it faces the dual challenges of sustaining development and combating climate change. The power sector is foundational to its economy and a key arena for reducing carbon emissions. Despite the Paris Agreement’s limited legal enforceability for specific commitments and its insufficient demands on emerging developing nations relative to their capabilities, Bangladesh has proactively sought to diminish fossil fuel reliance, cut emissions, and expand renewable energy share. This endeavor aims to build a nation conscious of green energy development, contributing to global climate governance. In this context, the solar system emerges as a central pillar for achieving these goals.

Bangladesh’s electricity industry is a strategically supported domain, crucial for poverty alleviation, national security, and economic growth. However, its energy resource endowment is poor, characterized by “rich gas, scarce coal, and lacking oil,” placing it as a net energy importer with a pronounced unidirectional international energy cooperation. It heavily depends on foreign technology and capital. Data from the Bangladesh Power Development Board (BPDB) for the fiscal year 2020-2021 show a total generation of approximately 80,423 GWh (including 8,103 GWh imported), with per capita generation and consumption at 475 kWh and 422 kWh, respectively. Yet, due to resource limitations and historical energy layouts, the current power structure is severely imbalanced, overly reliant on traditional fossil fuels like coal, oil, and gas, which collectively account for nearly 90%, while green, low-carbon renewable energy contributes only about 1%. This imbalance underscores the urgency for transition.

| Energy Source | Percentage (%) | Notes |

|---|---|---|

| Fossil Fuels (Coal, Oil, Gas) | ~90 | Dominant but unsustainable |

| Renewable Energy | ~1 | Primarily solar system contributions |

| Others (e.g., imports) | ~9 | Supplements local generation |

The need to adjust the generation mix is driven by depleting domestic fossil fuels, high import costs, and instability in direct electricity purchases from neighbors. Bangladesh must vigorously develop renewables, with the solar system playing a pivotal role, to provide safe, reliable, and affordable electricity. Over the past decade, the government has focused on expanding renewable energy exploitation. The 2008 Renewable Energy Policy targeted 10% of total electricity demand from renewables by 2021, but this goal has been overly optimistic. Even with revisions in the Eighth Five-Year Plan (2021-2025) extending the deadline to 2025, achieving 10% remains challenging. As of March 2022, renewable energy generation breakdown is as follows:

| Type | Off-grid (MW) | On-grid (MW) | Total (MW) | Percentage (%) |

|---|---|---|---|---|

| Solar System | 347.52 | 198.28 | 545.8 | 69.99 |

| Hydro | 0 | 230 | 230 | 29.50 |

| Wind | 2 | 0.9 | 2.9 | 0.37 |

| Biomass | 1.09 | 0 | 1.09 | 0.14 |

| Total | 350.61 | 429.18 | 779.79 | 100 |

Renewable energy has a long history in Bangladesh, dating back to hydropower projects in 1957. However, the solar system stands out as the largest renewable energy project, especially through Solar Home Systems (SHS), which have been instrumental in achieving near-universal electricity access. Considering the limitations of hydro, wind, and biomass, Bangladesh views solar energy, particularly photovoltaic (PV) power, as the top priority for future renewable development. The country’s geographical location in South Asia ensures ample sunshine year-round, with average daily solar radiation ranging from 4.0 to 6.5 kWh/m². This abundance enables significant energy potential, which can be quantified using the formula for solar energy potential:

$$ E = A \times I \times \eta \times t $$

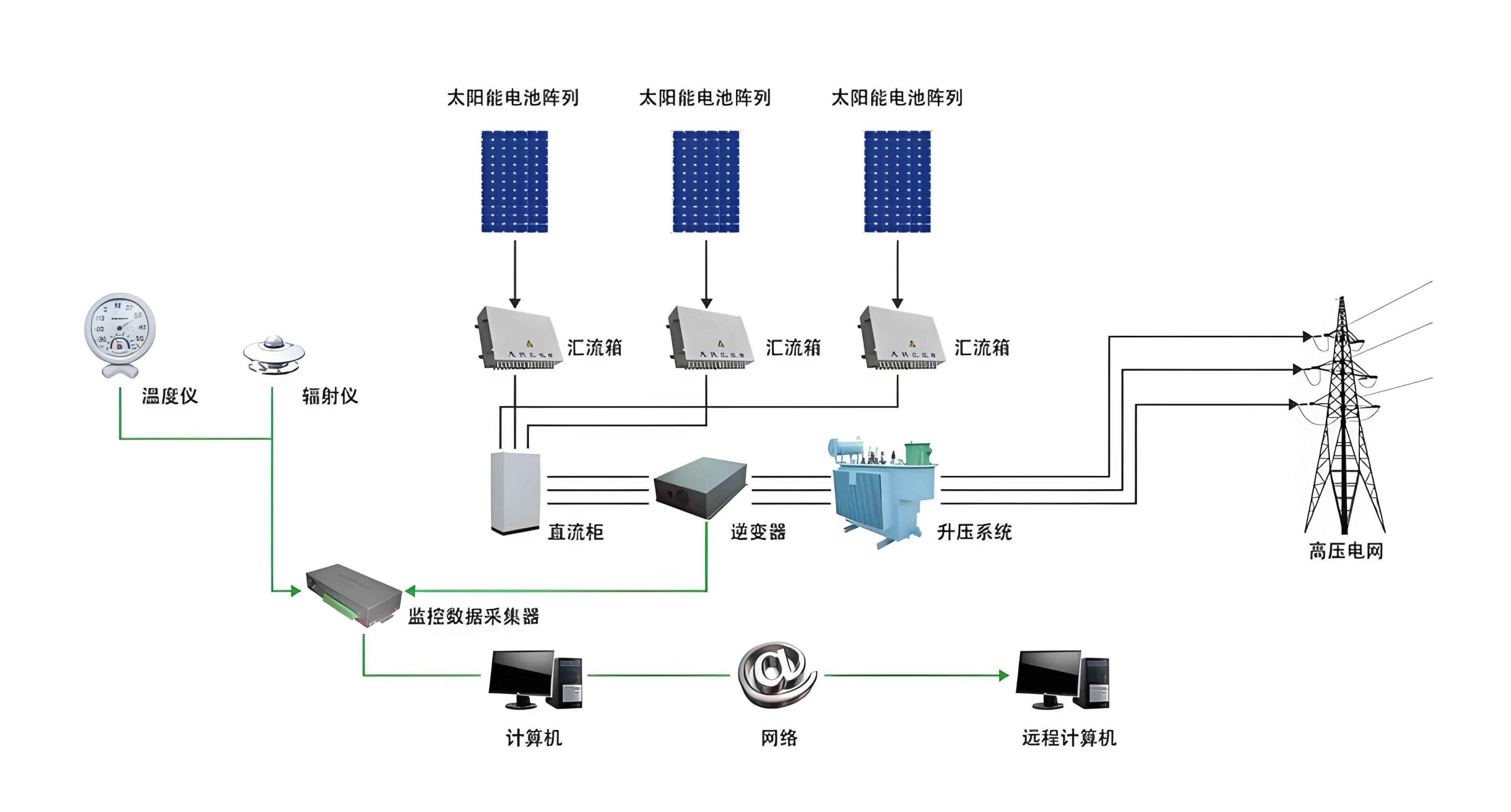

where \( E \) is the energy output, \( A \) is the area available for solar system installation, \( I \) is the solar irradiance, \( \eta \) is the efficiency of the PV panels, and \( t \) is the time. For Bangladesh, with an estimated land area suitable for solar farms, the potential is immense. The solar system can generate up to \( 10^{18} \) joules of energy annually, highlighting its viability for large-scale PV plants.

In recent years, Bangladesh has enacted policies to support solar system development, such as the Renewable Energy Policy, Sustainable and Renewable Energy Development Authority Act, Solar Power Development Project Implementation Guidelines, Bangladesh Delta Plan 2100, and the National Solar Energy Action Plan (2021-2041). Since June 2020, when the Prime Minister assumed the chair of the Climate Vulnerable Forum, Bangladesh has re-evaluated energy policies, emphasizing renewables. The “Mujib Climate Prosperity Plan” (MCPP) sets ambitious targets: by 2030, 12 solar projects will add 500 MW of solar power; by 2041, renewables should constitute 40% of the energy mix, aiding Bangladesh’s goal to become a developed nation. MCPP bridges existing policies, accelerating solar system deployment and marking a rapid development phase.

Current progress includes numerous PV projects approved or operational post-MCPP. For instance, the Narayanganj 100 MW, Feni 100 MW, Jamalpur 100 MW, and Sundarganj 280 MW projects have been signed, while others like Mymensingh 73 MW, Sirajganj 7.8 MW, Manikganj 35 MW, and Bagerhat 130 MW are already commercially operational. These initiatives demonstrate the growing momentum for solar system integration. However, the market has faced slow前期 progress due to several key issues.

First, land acquisition is a major hurdle. Bangladesh has a high population density, limited land area, and a private land ownership system, making consolidation difficult. Suitable sites for solar system projects, such as riverbanks, require land reclamation, increasing costs. BPDB’s tender requirements often mandate bidders to secure land, deterring participation. This land scarcity is a primary constraint for large-scale on-grid PV projects. Yet, evolving societal attitudes, technological advancements reducing land needs per unit of electricity, and integrated approaches like agrivoltaics or floating solar system can mitigate this over time.

Second, the policy framework is incomplete. While Bangladesh emphasizes renewable energy, policies often remain on paper, with inter-departmental conflicts and inefficient execution hindering synergy. Strong, consistent policy support and effective regulatory oversight are essential. Bangladesh should learn from international best practices, formulate scientific PV capacity plans, and adopt investor-friendly measures like adjusted project development models, optimized loan lock-in periods, improved capacity tariff mechanisms, and exemptions from import duties or value-added taxes. These steps would make solar system projects more feasible and sustainable.

Third, industrial配套 is落后. The solar system industry is a high-tech sector involving optics, semiconductors, chemicals, and machinery. Bangladesh lacks a domestic PV industrial cluster, with no local production in upstream raw materials (e.g., silicon), midstream cells and modules, or downstream applications. Consequently, all equipment, spare parts, and technical expertise for PV plant construction, operation, and maintenance are imported. The absence of local manufacturing,落后的 logistics, and shortage of skilled personnel pose significant challenges. Until Bangladesh can重塑产业逻辑 and achieve independent R&D, it must rely on external support to bridge gaps and drive solar system growth.

These factors lay the groundwork for enhanced cooperation between China and Bangladesh. The two nations share a strong bilateral relationship, aligned development goals, and strong economic-technological complementarity, offering vast合作 potential. As a traditional friendly neighbor, Bangladesh is a major recipient of Chinese aid and the first South Asian country to respond to the Belt and Road Initiative. Bilateral trade has grown rapidly, direct investment has expanded, and Chinese承包工程 has risen steadily. Bangladesh’s leaders have expressed eagerness to deepen产能合作 with China. Today, China is Bangladesh’s largest trading partner, while Bangladesh is China’s third-largest trading partner and engineering承包 market in South Asia. The power sector, a focus for Chinese enterprises, has seen successful布局 in Bangladesh, with some firms establishing strong brand presence.

Development goals are highly契合. Bangladesh’s “Golden Bangladesh Dream” (to become a middle-income country by 2021 and developed by 2041) aligns with China’s “Two Centenaries” goals. The elevation of bilateral relations to a strategic partnership in 2016明确了两国产能合作方向. Both countries prioritize协同推进 economic高质量发展和生态环境高水平保护, supporting energy结构转型. The solar system, as a representative renewable, is becoming a主力军 in the清洁低碳转型,助力实现 “dual-carbon” targets. Deepening solar system industry合作 can融通两国发展目标.

Economic-technological互补性 is strong. Bangladesh’s current level cannot independently sustain its梦想. As analyzed, it has ambitious goals for green energy转型 and solar system resource development but lacks resources in source-grid-load-storage,专业技术, talent, and capital. It needs support from产业成熟国家 like China. Bangladesh actively encourages foreign capital in power projects, offering a promising market, attractive labor resources, excellent credit信誉, and efforts to cultivate a favorable business environment and investor confidence. These aspects make Bangladesh an ideal destination for Chinese international产能合作.

Looking ahead, Bangladesh’s solar system market is poised for rapid growth over the next decade, transitioning to全面平稳发展阶段 in twenty years. Chinese enterprises should formulate “going global” strategies based on their strengths, assessing Bangladesh’s business environment, accurately研判项目模型, and innovating合作模式 (e.g., BOT/PPP). Opportunities in投融资, equipment export, technical咨询, and劳务合作 should be sought. By leveraging advanced technology, management mechanisms, talented teams, and a win-win philosophy, they can contribute to Bangladesh’s solar system development,助力当地经济发展, undertake corporate social responsibility, and achieve shared economic循环.

In conclusion, the solar system is not just a technological solution but a transformative force for Bangladesh’s energy future. By addressing challenges through政策完善, industrial升级, and international合作, Bangladesh can harness its solar potential to build a sustainable and prosperous economy. The journey requires collective effort, but with the solar system at its core, a greener tomorrow is within reach.