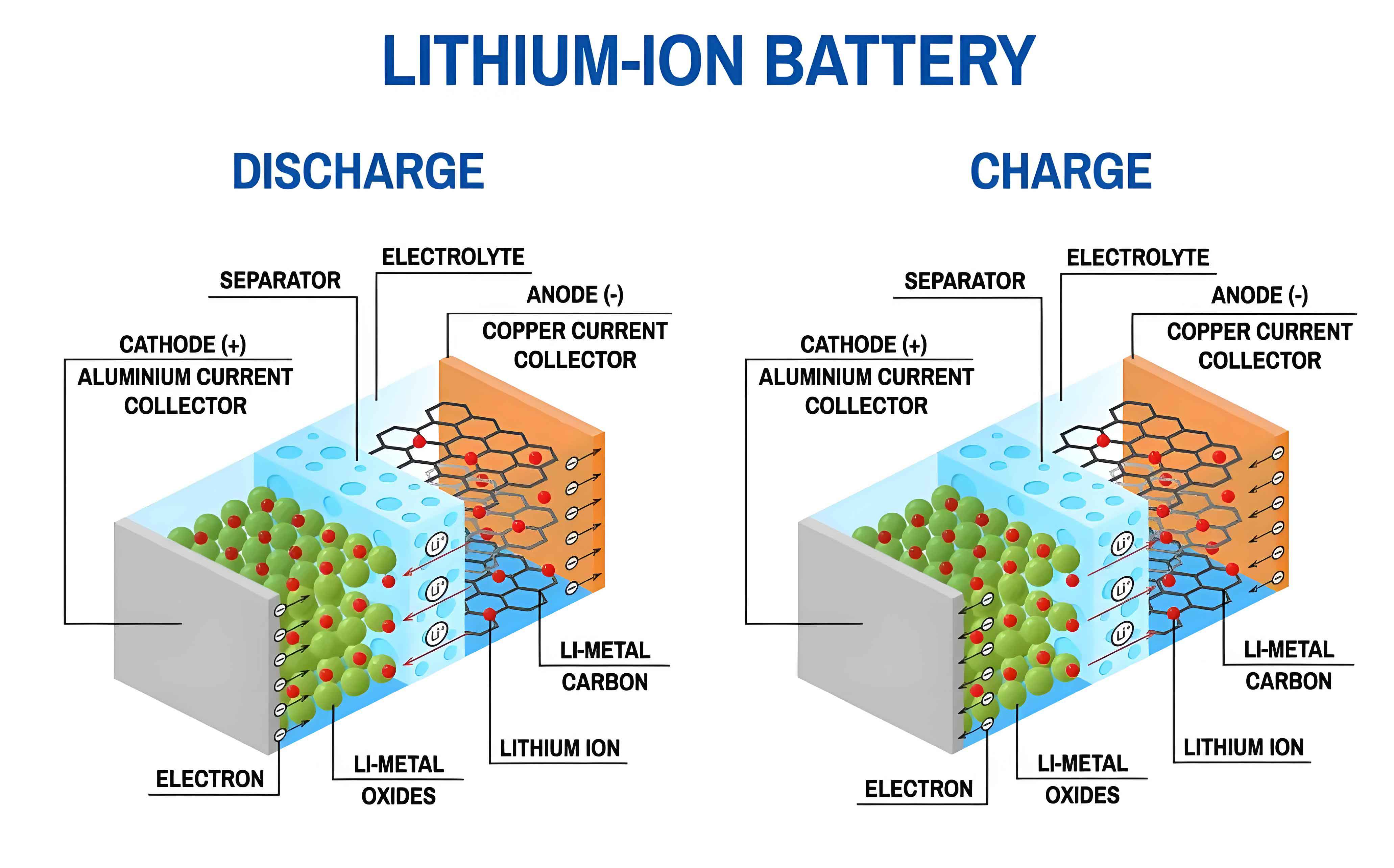

The global imperative to mitigate climate change has catalyzed a profound shift towards low-carbon economic models. At the heart of this transformation lies the critical need to decarbonize energy generation and consumption. This transition is fundamentally reliant on two interconnected pillars: the electrification of transport and the integration of intermittent renewable energy sources like solar and wind into stable power grids. Both pillars converge on a single, indispensable technological enabler—the energy storage system, with the lithium-ion battery reigning supreme as the dominant solution. As a researcher deeply engaged in this field, I observe that the evolution of the lithium-ion battery industry is not merely a market trend but a central force sculpting our sustainable future. This article provides an in-depth analysis of the lithium-ion battery industry’s current state, its pivotal role in enabling low-carbon economies, the multifaceted challenges it confronts, and its promising trajectory, enriched with quantitative summaries through tables and formulas.

The Imperative of Low-Carbon Development and the Energy Storage Nexus

The concept of a low-carbon economy is predicated on decoupling economic growth from greenhouse gas (GHG) emissions. This involves a systemic overhaul of energy infrastructure, prioritizing efficiency, renewable sources, and circularity. The transportation sector, historically dependent on internal combustion engines, and the power sector, reliant on fossil-fuel-based peaker plants for grid stability, are primary targets for decarbonization. The integration of variable renewable energy (VRE) sources creates a mismatch between supply and demand, necessitating robust energy storage to ensure grid reliability and maximize clean energy utilization. Herein lies the critical function of the lithium-ion battery. Its superior characteristics—high energy density, high power density, declining cost, and improving longevity—make it the technology of choice for mobile (electric vehicles) and stationary (grid storage) applications. The growth trajectory of the lithium-ion battery industry is therefore intrinsically linked to the pace and success of the global low-carbon transition.

State of the Global Lithium-Ion Battery Industry: A Quantitative Snapshot

The lithium-ion battery industry has experienced exponential growth over the past decade, driven by policy mandates and market pull. The industry landscape is characterized by rapid capacity expansion, intense innovation, and evolving geopolitical dynamics.

Production Capacity and Market Leadership

Global manufacturing capacity for lithium-ion batteries is heavily concentrated in Asia, with China commanding a dominant share. This leadership is the result of strategic national policy, extensive supply chain integration, and massive investments in gigafactories. Other regions, notably Europe and North America, are aggressively building local capacity to secure supply chain resilience and capture economic value. The following table summarizes the estimated capacity landscape and primary drivers.

| Region/Country | Estimated Share of Global Li-ion Battery Manufacturing Capacity (2024) | Key Growth Drivers & Policies |

|---|---|---|

| China | ~70-75% | Long-term strategic planning, complete domestic supply chain, subsidies for NEVs, export strength. |

| Europe | ~10-15% | European Green Deal, stringent CO2 emission standards, CBAM, incentives for local gigafactories. |

| United States | ~5-10% | Inflation Reduction Act (IRA) tax credits, mandates for domestic content and sourcing. |

| South Korea & Japan | ~10% (combined) | Advanced chemical and manufacturing expertise, strong IP portfolio, global OEM partnerships. |

Technological Evolution: Beyond Incremental Gains

Innovation in lithium-ion battery technology is relentless, focusing on the “iron triangle” of performance: energy density, cost, and safety/lifetime. Progress is achieved through advancements in cell chemistry and system-level engineering.

- Energy Density: The quest for longer-range EVs pushes the limits of gravimetric and volumetric energy density. This is pursued via high-nickel NCM/NCA cathodes (e.g., NCM811, NCA), silicon-blended anodes, and cell-to-pack (CTP) structural designs that reduce inactive material. The theoretical energy density $$E_{cell}$$ can be approximated by the contributions of cathode and anode materials:

$$E_{cell} \approx \frac{C_{cathode} \times V_{cathode} \times m_{cathode} + C_{anode} \times V_{anode} \times m_{anode}}{m_{cell}}$$

where $$C$$ is specific capacity, $$V$$ is operating voltage, and $$m$$ is mass. The industry’s roadmap points towards solid-state batteries, which replace the flammable liquid electrolyte with a solid conductor, promising a step-change in energy density (potentially >500 Wh/kg) and intrinsic safety. - Cost Reduction: The dramatic fall in lithium-ion battery pack prices, from over $1,100/kWh in 2010 to around $139/kWh in 2023, is a cornerstone of the EV revolution. This reduction follows a learning curve, often modeled as:

$$P_t = P_0 \times (C_t)^{-\alpha}$$

where $$P_t$$ is the price at cumulative production $$C_t$$, $$P_0$$ is the initial price, and $$\alpha$$ is the learning rate (empirically ~18-20% for lithium-ion batteries). Future cost reductions will come from manufacturing scale, process innovation (e.g., dry electrode coating), and lower raw material costs via recycling. - Cycle Life and Safety: Extending battery life reduces total cost of ownership for both EVs and storage. Cycle life $$N$$ is influenced by operational parameters:

$$N \propto \frac{1}{(\Delta DOD)^{\beta} \cdot (C-rate)^{\gamma} \cdot \exp(\frac{-E_a}{kT})}$$

where $$\Delta DOD$$ is depth of discharge, $$C-rate$$ is charge/discharge current, $$E_a$$ is activation energy, $$k$$ is Boltzmann’s constant, and $$T$$ is temperature. Advanced Battery Management Systems (BMS) using sophisticated algorithms and sensors are crucial for managing these parameters, preventing thermal runaway, and ensuring safety.

The Enabling Role of Lithium-Ion Batteries in Low-Carbon Sectors

1. Decarbonizing Transportation: The Electric Vehicle Revolution

The lithium-ion battery is the definitive enabler of modern electric vehicles. The lifecycle GHG emissions of a battery electric vehicle (BEV) are significantly lower than those of an internal combustion engine vehicle (ICEV), even when accounting for battery manufacturing. The carbon reduction intensifies as the grid becomes cleaner. The lithium-ion battery’s performance directly dictates EV adoption metrics: driving range, charging time, and purchase price. Continuous improvement in these areas is breaking down consumer barriers. Furthermore, the rise of EVs creates a synergistic opportunity for vehicle-to-grid (V2G) services, where parked EVs could act as distributed energy resources, providing grid stability and integrating more renewables.

2. Stabilizing the Green Grid: Stationary Energy Storage Systems (ESS)

As the share of solar and wind power grows, the grid requires flexible resources to balance supply and demand. Lithium-ion battery-based ESS provides a fast-responding, modular, and scalable solution for multiple grid services:

- Frequency Regulation: Injecting or absorbing power in sub-second response to maintain grid frequency.

- Renewable Energy Time-Shift (Arbitrage): Storing excess solar energy during the day for use in the evening peak.

- Peak Shaving: Reducing demand on the grid during periods of highest usage, deferring costly infrastructure upgrades.

- Backup Power: Providing uninterrupted power supply for critical infrastructure.

The economic value $$V_{ESS}$$ of a grid-scale lithium-ion battery system can be decomposed into the revenue from these stacked services:

$$V_{ESS} = \sum_{i=1}^{n} (R_{service_i} \times A_{service_i}) – (C_{cap} + C_{O\&M} + C_{degr})$$

where $$R$$ is revenue rate, $$A$$ is available capacity for service $$i$$, $$C_{cap}$$ is capital cost, $$C_{O\&M}$$ is operation & maintenance cost, and $$C_{degr}$$ is degradation cost.

3. Beyond Mobility and Grid: Diversifying Applications

The versatility of the lithium-ion battery extends to numerous other sectors crucial for a low-carbon society:

| Application Sector | Role in Low-Carbon Transition | Specific Requirements |

|---|---|---|

| Marine & Aviation | Electrification of short-sea shipping, ferries, and small aircraft; hybrid systems for larger vessels to reduce fuel consumption and port emissions. | Extreme safety, high energy density, tolerance to vibration and harsh environments. |

| Consumer Electronics & IoT | Enabling portable, cordless devices, reducing electronic waste through longer lifespan and replaceable power sources. | Miniaturization, high volumetric energy density, flexible form factors. |

| Off-Grid & Residential Storage | Empowering energy independence, maximizing self-consumption of rooftop solar, and enhancing resilience against grid outages. | Safety for home use, long cycle life, ease of installation, and smart energy management integration. |

Critical Challenges and Risks on the Path Forward

Despite its promise, the lithium-ion battery industry faces significant headwinds that could constrain its growth and environmental benefits.

1. Raw Material Supply Chain Vulnerabilities

The lithium-ion battery supply chain is geopolitically sensitive and subject to volatile prices. Key materials like lithium, cobalt, nickel, and graphite are mined in a limited number of countries. Supply concentration risks, coupled with surging demand, lead to price instability, as seen in the 2021-2022 lithium price spike. Furthermore, mining and processing these materials often involve significant environmental and social governance (ESG) challenges, including water usage, habitat destruction, and labor practices. The carbon footprint of upstream activities (mining, refining) constitutes a substantial portion of the total lifecycle emissions of a lithium-ion battery, presenting a paradox that the industry must solve.

2. Technological and Manufacturing Hurdles

While incremental improvements continue, fundamental chemistry limits for conventional liquid electrolyte lithium-ion batteries are approaching. Breakthroughs like solid-state technology face formidable manufacturing and cost barriers before commercialization at scale. Furthermore, rapid industry expansion risks creating structural overcapacity for older technology generations while leading firms race to deploy newer, more efficient designs. This dynamic can lead to stranded assets and intense price wars.

3. The End-of-Life Imperative: Recycling and Second-Life

A truly sustainable lithium-ion battery ecosystem requires a closed-loop material cycle. Currently, recycling rates remain low due to technical complexity, collection logistics, and economic viability. However, effective recycling is crucial to:

- Mitigate supply risks for critical minerals.

- Reduce the lifecycle environmental impact (e.g., GHG emissions from primary production).

- Prevent environmental contamination from improper disposal.

Simultaneously, repurposing used EV batteries for less demanding second-life applications (e.g., stationary storage) can extend their utility before recycling. The economic model for a circular lithium-ion battery economy is still being proven at scale.

4. Evolving Regulatory and Trade Landscape

New regulations, particularly in the European Union, are setting stringent sustainability benchmarks. The EU Battery Regulation mandates comprehensive carbon footprint declarations, minimum recycled content targets, due diligence on raw material sourcing, and battery passport requirements. Similarly, the US Inflation Reduction Act ties tax credits to domestic manufacturing and sourcing requirements. These policies act as both drivers for greener practices and potential non-tariff trade barriers, forcing global lithium-ion battery producers to adapt their supply chains and operational transparency rapidly.

Prospects and Strategic Pathways for a Sustainable Lithium-Ion Battery Industry

Overcoming these challenges requires concerted efforts across technology, policy, and business models. The future outlook for the lithium-ion battery industry in supporting a low-carbon economy remains profoundly positive, contingent on strategic navigation.

1. Technology and Cost Trajectory: The Road to $100/kWh and Beyond

The learning curve for lithium-ion batteries is expected to continue, with pack prices potentially falling below $100/kWh by the end of the decade. This will make EVs price-competitive with ICEVs without subsidies and unlock massive new markets for grid storage. Technological progress will be multi-pronged:

- Next-Generation Chemistries: Commercialization of silicon-dominant anodes, lithium-metal anodes (in solid-state configurations), and cobalt-free cathodes (e.g., LMFP – Lithium Manganese Iron Phosphate).

- Manufacturing Revolution: Adoption of dry-process electrode manufacturing, which eliminates energy-intensive drying ovens and toxic solvent use, thereby cutting cost, factory footprint, and carbon emissions.

- Smart Battery Systems: Integration of AI and digital twins for predictive health management, optimal charging, and safety assurance, maximizing value over the battery’s life.

2. Supply Chain Resilience and Circularity

Future strategies will emphasize diversification and localization of supply chains for geopolitical security. More importantly, the circular economy will transition from an ideal to an operational necessity. Investments in advanced recycling technologies (direct recycling, hydrometallurgy) will increase recovery rates of valuable materials. Policy will drive this through extended producer responsibility (EPR) schemes and recycled content mandates. The economic equation for recycling will improve as scale increases, material prices remain elevated, and regulation internalizes environmental costs.

3. Deepening Sector Coupling and System Integration

The role of the lithium-ion battery will evolve from a standalone component to an integrated node within smarter energy systems. Key trends include:

- Vehicle-to-Everything (V2X): Widespread deployment of V2G, vehicle-to-home (V2H), and vehicle-to-load (V2L) technologies, turning the EV fleet into a dynamic grid asset.

- Renewables-Plus-Storage as the New Baseload: Co-location of large-scale lithium-ion battery storage with solar and wind farms will become the standard model for new renewable projects, providing firm, dispatchable clean power.

- Industrial and Commercial Microgrids: Lithium-ion batteries will be central to microgrids for factories, campuses, and data centers, improving efficiency, reliability, and renewable consumption.

4. Navigating the Green Trade and Policy Environment

Proactive adaptation to new sustainability regulations will be a key competitive differentiator. Leading lithium-ion battery manufacturers will:

- Implement robust, auditable lifecycle assessment (LCA) and carbon accounting across their supply chains.

- Develop “green” battery products with lower embedded carbon, enabled by renewable-powered manufacturing and recycled materials.

- Engage in international standard-setting to harmonize metrics like carbon footprint calculation and battery passport data formats, reducing trade friction.

In conclusion, the lithium-ion battery industry stands at a pivotal juncture. It is the cornerstone technology for electrifying transport and greening the grid—the two most critical fronts in the battle against climate change. While formidable challenges related to resources, technology, and sustainability persist, the trajectory of innovation, cost reduction, and systemic integration points toward a future where the lithium-ion battery is ubiquitous and essential. Its continued evolution, guided by principles of circularity and decarbonized production, will be instrumental in transitioning from a fossil-fuel-based economy to a resilient, efficient, and truly low-carbon global society. The journey of the lithium-ion battery, therefore, is far more than an industrial narrative; it is fundamentally the story of how we power our sustainable future.