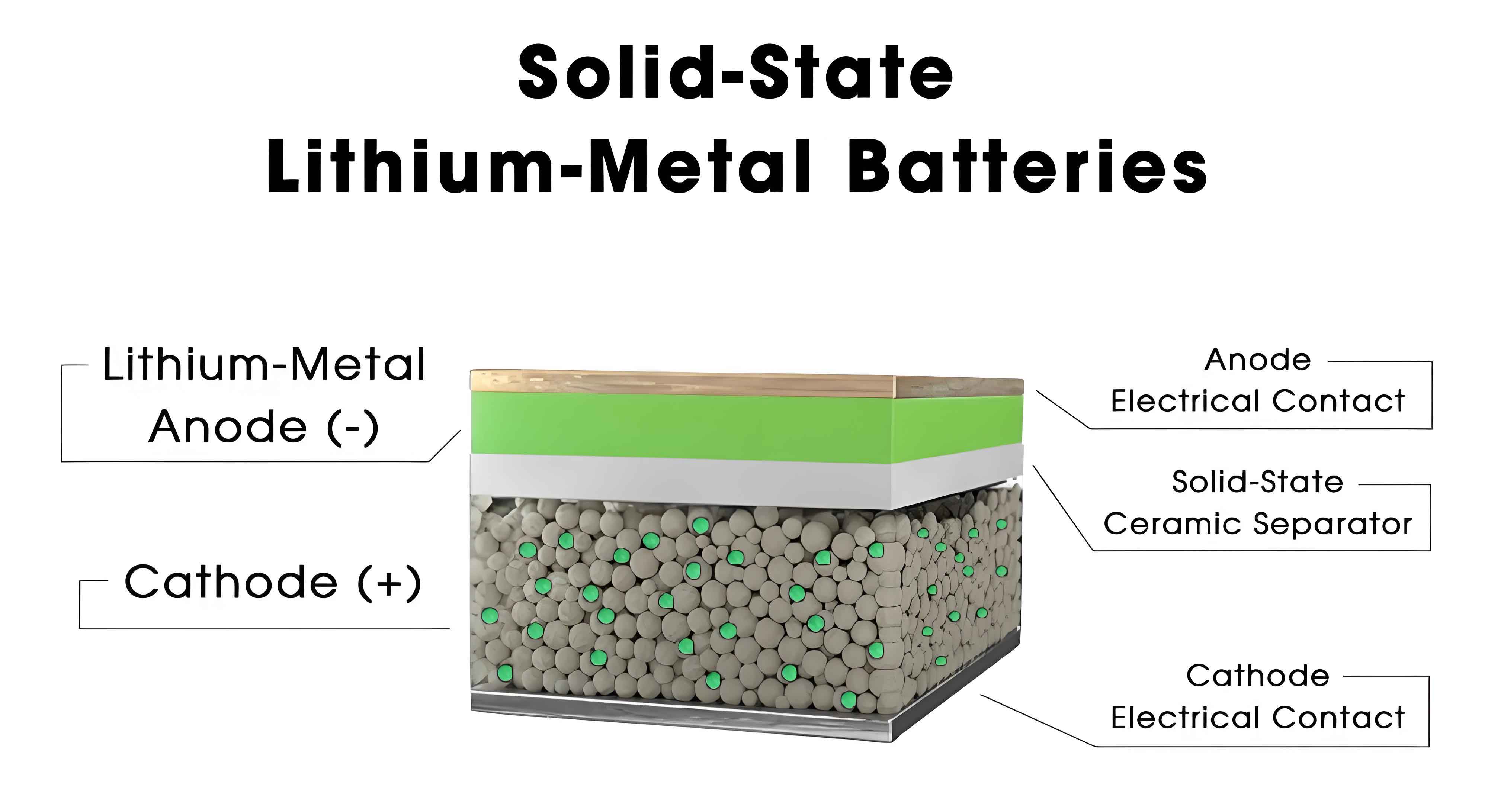

As a keen observer of the automotive and energy storage industries, I have witnessed the rising tide of solid-state battery development sweep across the globe. This technological frontier, promising revolutionary improvements in energy density and safety, has ignited intense competition among major economic regions. While China’s产业链 is advancing rapidly, the approaches and progress in Japan, South Korea, Europe, and America present a fascinating mosaic of strategies, technical preferences, and commercialization timelines. In this comprehensive analysis, we will delve deep into the current state of solid-state battery research and development outside China, exploring the distinct paths taken by these regions, the key players involved, and the scientific and economic factors shaping this race. We will employ tables and formulas to succinctly summarize complex data and technical parameters, aiming to provide a clear picture of where the global solid-state battery landscape stands today.

The fundamental promise of the solid-state battery lies in its replacement of the flammable liquid electrolyte found in conventional lithium-ion batteries with a solid electrolyte. This shift potentially eliminates leakage risks, enables the use of high-capacity lithium metal anodes, and allows for higher operating voltages. The overarching benefits can be summarized by enhancements in key metrics. For instance, the volumetric energy density (energy per unit volume) and gravimetric energy density (energy per unit mass) are expected to see significant leaps. These can be expressed as:

$$ E_v = \frac{C \times V}{A \times t} \quad \text{and} \quad E_g = \frac{C \times V}{m} $$

where \(E_v\) is volumetric energy density (Wh/L), \(E_g\) is gravimetric energy density (Wh/kg), \(C\) is capacity (Ah), \(V\) is average discharge voltage (V), \(A\) is electrode area (m²), \(t\) is thickness (m), and \(m\) is mass (kg). The solid-state battery aims for \(E_g\) values exceeding 500 Wh/kg, a substantial jump from the current 250-300 Wh/kg of advanced liquid lithium-ion cells.

The core technical differentiation among solid-state battery prototypes revolves around the choice of solid electrolyte material. The three primary families are polymer, oxide, and sulfide-based electrolytes, each with distinct properties that influence the technical route chosen by developers.

Polymer Electrolytes: These are typically composed of complexes like PEO (Polyethylene Oxide) with lithium salts. Their main advantage is relatively good flexibility and easier manufacturing processes akin to existing battery technology. However, their ionic conductivity (\(\sigma_i\)) is generally lower and highly temperature-dependent, often requiring operation above 60°C. The conductivity can be modeled by the Vogel-Tammann-Fulcher (VTF) equation:

$$ \sigma_i = A T^{-1/2} \exp\left(-\frac{B}{T – T_0}\right) $$

where \(A\) and \(B\) are constants, \(T\) is temperature, and \(T_0\) is the ideal glass transition temperature. This temperature sensitivity is a significant drawback for automotive applications.

Oxide Electrolytes: Materials like LLZO (Lithium Lanthanum Zirconium Oxide) offer high ionic conductivity and excellent stability against lithium metal. However, they are often brittle, leading to high interfacial resistance with electrodes. The ionic conduction in these crystalline materials often follows an Arrhenius-type behavior:

$$ \sigma_i = \sigma_0 \exp\left(-\frac{E_a}{k_B T}\right) $$

where \(\sigma_0\) is a pre-exponential factor, \(E_a\) is the activation energy for ion hopping, and \(k_B\) is Boltzmann’s constant.

Sulfide Electrolytes: Compounds such as LGPS (Li10GeP2S12) exhibit exceptionally high room-temperature ionic conductivity, sometimes rivaling that of liquid electrolytes (exceeding 10-2 S/cm). Their soft mechanical properties allow for better interfacial contact. Yet, they are highly sensitive to moisture, releasing toxic H2S upon exposure, which complicates production. Their conductivity often stems from a disordered structure facilitating lithium ion migration.

The global competition in solid-state battery development is not just a scientific endeavor but a strategic industrial race. Different regions have coalesced around preferred technical routes, influenced by historical expertise, corporate alliances, and national industrial policies. The commitment levels and public declarations also vary significantly, painting a picture of determined advancement in some areas and more cautious, investment-driven exploration in others.

Japan and South Korea have emerged as the most vocal and coordinated blocs pursuing the solid-state battery future. Their focus is predominantly on the sulfide-based solid-state battery, believed to offer the best long-term performance for electric vehicles.

In Japan, the effort is characterized by early starts, extensive patent portfolios, and strong government-industry collaboration. A major automotive manufacturer, often cited as a leader in patent filings, has been researching solid-state batteries since the 1990s and aims to commercialize sulfide-based cells by 2030. Another major electronics corporation has also developed prototypes and targets production by the end of this decade. The national strategy is clear. Government-backed organizations have launched large-scale consortium projects involving dozens of companies, providing substantial funding for research into next-generation batteries, including the solid-state battery. A key national policy document outlines ambitious goals for domestic and global battery production capacity, explicitly targeting the commercial application of all-solid-state lithium batteries around 2030. Furthermore, critical supply chain elements are being secured, such as the establishment of multi-ton per year production lines for sulfide solid electrolyte materials by specialized chemical companies.

South Korea’s approach leverages the immense scale and expertise of its flagship battery manufacturers. All three major players have announced detailed roadmaps for solid-state battery development, primarily along the sulfide and hybrid polymer routes. One aims to start mass production of all-solid-state batteries by 2027, another targets commercialization of improved-safety polymer-based semi-solid batteries by 2026, and the third plans for mass production in 2028. The national government has pledged massive joint investment with these companies to develop advanced battery technologies, including the solid-state battery, aiming for early commercialization. The synergy between Japanese automotive OEMs and Korean battery giants in this sulfide domain is a formidable combination, covering everything from material science to cell manufacturing and vehicle integration.

The landscape in Europe and America appears more fragmented and driven by strategic partnerships between automakers and specialized startups, with a broader mix of technical routes.

European automakers have shown interest but with noticeable caution regarding the immediate necessity of solid-state battery technology. Some executives have publicly questioned its imperative, citing rapid improvements in conventional lithium-ion chemistry. Nonetheless, virtually all major premium carmakers are hedging their bets through investments in American solid-state battery startups. For instance, one German auto giant is the largest shareholder in a startup focusing on oxide-based solid-state batteries, which has demonstrated impressive cycle life in tests—reporting over 500,000 kilometers with minimal capacity fade. The partnership aims to establish a pilot production line by 2025. Another major manufacturer has received early prototype samples (A-samples) from a startup developing sulfide-based cells, with a goal for量产 by 2026. A third luxury brand has invested in a different startup and has recently received more mature B-sample cells for testing. The European approach seems to be one of “wait-and-see” coupled with strategic stakes in promising technologies, rather than a full-throttle, national-level industrial push.

In the United States, innovation is largely spearheaded by venture-capital-funded startups, each championing different solid-state battery chemistries. These companies have become the primary vessels for European and sometimes Asian automotive investment. Beyond the oxide and sulfide pioneers mentioned, other startups are exploring proprietary polymer or composite systems. The U.S. Department of Energy also funds research, but the ecosystem is less centralized than in East Asia. The progress is measured in milestone achievements: delivering sample cells to automotive partners, scaling up layer counts, and demonstrating performance metrics like energy density and cycle life. The formula for success here combines scientific breakthrough with the ability to scale manufacturing processes cost-effectively, a challenge often summarized by the need to reduce the cost per kilowatt-hour (\(C_{kWh}\)).

$$ C_{kWh} = \frac{C_{materials} + C_{processing} + C_{capital}}{E \times \eta \times yield} $$

where \(C_{materials}\), \(C_{processing}\), and \(C_{capital}\) are costs related to materials, manufacturing processes, and capital investment, \(E\) is the energy per cell, \(\eta\) is efficiency, and \(yield\) is production yield. For solid-state batteries, \(C_{materials}\) for novel electrolytes and lithium metal, and \(C_{processing}\) for controlled dry rooms or specialized coating, are currently high.

To systematically compare the global efforts, the following tables consolidate the technical focus and announced progress of key players from Japan, South Korea, Europe, and America. It is crucial to note that these timelines are aspirational and subject to the resolution of significant technical hurdles.

| Region | Company / Entity | Primary Solid-State Battery Electrolyte Route | Key Development Milestones & Commercialization Targets |

|---|---|---|---|

| Japan | Major Automotive Manufacturer A | Sulfide | Extensive patent holder. Targets vehicle integration of sulfide solid-state battery by 2030. Reported breakthroughs in durability and fast-charging performance in 2023. |

| Major Electronics Corporation B | Sulfide | Publicly demonstrated prototype cell in 2023. Plans for mass production of solid-state battery before 2030. | |

| Automotive Manufacturer C | Sulfide | Plans pilot production line for solid-state battery in 2025. Aims to launch EV model powered by all-solid-state battery around 2028. | |

| Chemical Company D | Sulfide (Materials) | Established a production line with capacity of several tons per year for sulfide solid electrolyte, supplying key material for domestic solid-state battery development. | |

| South Korea | Battery Maker E | Sulfide, Polymer | Completed a pilot line for all-solid-state battery in 2023. Aims to develop large-format cell production tech by 2025, targeting mass production in 2027. |

| Battery Maker F | Sulfide, Polymer | Built semi-solid battery production line in 2023. Targets commercialization of an improved-safety polymer-based semi-solid-state battery by 2026. Aims for full solid-state battery later. | |

| Battery Maker G | Sulfide | Plans to complete early prototypes by 2026 and achieve mass production of solid-state battery by 2028. |

The collective drive in Asia is underpinned by national strategies and large-scale corporate R&D. In contrast, the transatlantic collaboration model is evident in the next table.

| Region | Company / Entity | Primary Solid-State Battery Electrolyte Route | Key Development Milestones & Commercialization Targets |

|---|---|---|---|

| Europe | Automotive Group H (German) | Oxide (via partnership) | Major investor in American Startup J. Completed endurance tests showing ultra-long life. Plans for a solid-state battery production line by 2025 via the startup. |

| Automotive Manufacturer I (German) | Sulfide (via partnership) | Received first A-sample cells from American Startup K in 2023 for vehicle integration tests. Aims for production around 2026. | |

| Automotive Brand L (German) | Composite/Polymer (via partnership) | Investor in American Startup M. Received advanced B-sample solid-state battery cells for testing in 2024. No firm public量产 timeline. | |

| America | Startup J | Oxide | Developer of oxide-based solid-state battery cell. Reported exceptional cycle life data. Targets pilot line construction by 2025. |

| Startup K | Sulfide | Developer of sulfide-based solid-state battery. Delivered first A-samples to automotive partners. Aims for量产 readiness by 2026. | |

| Startup M | Proprietary | Developer of solid-state battery technology. Delivered >106 Ah B-sample cells to automotive partner in 2024 for validation. |

Beyond corporate roadmaps, the scientific and engineering challenges remain immense. The performance of a solid-state battery is not just about the electrolyte. The interfaces between the solid electrolyte and the electrodes (cathode and anode) are critical bottlenecks. High interfacial resistance (\(R_{int}\)) can cripple power performance and cycle life. This resistance arises from poor physical contact, chemical reactions, and space-charge layers. The total cell impedance (\(Z_{cell}\)) can be approximated as the sum of bulk and interfacial components:

$$ Z_{cell} = R_{bulk} + R_{int,cathode} + R_{int,anode} + Z_{W} $$

where \(R_{bulk}\) is the resistance of the electrolyte bulk, \(R_{int}\) are the interfacial resistances, and \(Z_{W}\) is the Warburg impedance related to diffusion. For lithium metal anodes, the challenge includes suppressing dendrite growth through the solid electrolyte, which relates to the critical current density (\(i_{crit}\)) a cell can withstand before short-circuit. This is a key safety metric for the solid-state battery.

Manufacturing is another monumental hurdle. Coating thin, defect-free layers of brittle ceramics or handling moisture-sensitive sulfides requires entirely new production ecosystems. The cost equation mentioned earlier is daunting. A simplified comparison of estimated cost contributors for different solid-state battery types versus incumbent lithium-ion is illustrative, though precise numbers are closely guarded secrets.

| Battery Type | Primary Cost Drivers | Major Technical Hurdles | Manufacturing Complexity |

|---|---|---|---|

| Liquid Lithium-ion | Cathode materials (Ni, Co), LiPF6 electrolyte, Cu/Al foil | Energy density ceiling, thermal runaway risk | Mature, but drying and electrolyte filling are sensitive steps. |

| Polymer-based Solid-State Battery | Specialized polymer/salt complexes, possibly Li metal foil | Low conductivity at room temperature, limited voltage window | Potentially similar to existing roll-to-roll processes, but may require heating. |

| Oxide-based Solid-State Battery | LLZO-type ceramics, high-purity precursors, Li metal anode | Brittleness, high interfacial resistance, sintering energy cost | High. May require ceramic sintering furnaces, dry rooms, and precise lamination. |

| Sulfide-based Solid-State Battery | Ge, P, S raw materials, inert atmosphere processing, Li metal | Moisture sensitivity (H2S risk), interfacial stability, Li dendrite penetration | Very high. Entire production line must be in ultra-dry environment (dew point < -50°C). |

The divergence in regional strategies can be partly explained by risk assessment and industrial structure. The concerted, sulfide-focused push in Japan and Korea suggests a belief in a definitive technological victory and a willingness to invest heavily to overcome the associated severe challenges. It is a high-risk, high-reward strategy aiming for a dominant position in the next generation of battery technology. Their early lead in fundamental patents provides some cushion, but the path to cost-effective, high-volume manufacturing is long.

On the other hand, the European-American model appears more opportunistic and diversified. By investing in multiple startups across different chemistries, automakers spread their risk. Their public caution may stem from the impressive ongoing evolution of liquid lithium-ion batteries, whose energy density continues to improve through silicon-anodes, high-nickel cathodes, and cell-to-pack technologies. The incremental gain offered by an early, potentially expensive polymer solid-state battery might not justify the switch. Therefore, they are positioned to accelerate quickly if one of the startup technologies, like the oxide-based solid-state battery showing remarkable longevity, proves manufacturable at scale.

From my perspective, the global race for the solid-state battery is entering a critical phase. The next five years will likely see the transition from laboratory prototypes and small pilot lines to larger-scale validation in automotive testing programs. The key metrics to watch will be the scaling of layer counts and cell formats, the achievement of targeted cycle life (e.g., >1000 cycles with >80% capacity retention) under realistic conditions, and, most importantly, the demonstration of viable manufacturing costs. The performance of a solid-state battery in a real vehicle environment—subject to vibrations, temperature extremes, and fast charging—will be the ultimate test.

In conclusion, the development of the solid-state battery is a complex, multi-faceted global endeavor. Japan and South Korea are charging ahead with focused, nationally-backed strategies centered on the high-performance sulfide solid-state battery. Europe and America are pursuing a more distributed, partnership-driven approach, keeping multiple technology options alive while cautiously evaluating the timing of the technology’s necessity and economic viability. As the competition intensifies, cross-regional learning and potential collaboration in standardizing testing or addressing supply chain issues may emerge. Regardless of the path, the pursuit of the solid-state battery remains one of the most dynamic and consequential technological quests in the energy storage and automotive sectors today, with the potential to redefine performance and safety standards for electric mobility and beyond. The repeated emphasis on the solid-state battery throughout this analysis underscores its central role in this transformation. The coming years will reveal whether the bold, integrated strategies of East Asia will pay off first, or if the agile, startup-driven innovations nurtured in the West will leapfrog to commercialization. What is certain is that the journey towards the practical solid-state battery will continue to be a fascinating spectacle of science, engineering, and industrial strategy.