As an analyst deeply engaged in the energy storage sector, I have witnessed the transformative role of the lithium-ion battery industry in shaping the global transition to sustainable energy. From powering electric vehicles to enabling grid-scale storage, lithium-ion batteries have become indispensable in modern economies. In this article, I will delve into the intricate dynamics of the lithium-ion battery ecosystem, examining its cost structures, market trends, and future trajectories. My aim is to provide a holistic perspective that underscores the critical factors driving this industry forward.

The evolution of the lithium-ion battery industry is a testament to technological innovation and market demand. Since the commercial introduction of lithium-ion batteries in the early 1990s, advancements in energy density, cycle life, and cost reduction have propelled their adoption across diverse sectors. I recall that initially, consumer electronics like smartphones and laptops were the primary drivers, but today, the landscape has shifted dramatically. The surge in electric vehicle (EV) production and the integration of renewable energy sources have positioned lithium-ion batteries as a cornerstone of the clean energy revolution. From my analysis, the lithium-ion battery market is not just growing; it is evolving rapidly, with new applications emerging in areas such as aerospace, medical devices, and even deep-sea exploration. This expansion underscores the versatility and importance of lithium-ion battery technology.

To understand the lithium-ion battery industry, it is essential to first explore its applications. In consumer electronics, lithium-ion batteries provide the backbone for portable devices, offering high energy density and reliability. In transportation, the rise of electric vehicles has been a game-changer, with lithium-ion batteries enabling longer ranges and faster charging times. Moreover, energy storage systems (ESS) rely on lithium-ion batteries to balance grid loads, store excess renewable energy, and enhance power quality. From my observations, the demand for lithium-ion batteries in ESS is accelerating, driven by global commitments to decarbonize energy grids. Additionally, niche sectors like drones and wearable technology are increasingly adopting lithium-ion batteries, highlighting their pervasive influence. The lithium-ion battery, therefore, is not a single-product solution but a multifaceted technology that adapts to various energy needs.

Turning to the industrial chain, the lithium-ion battery ecosystem can be segmented into upstream raw materials, midstream manufacturing, and downstream applications, along with a growing recycling sector. I will analyze each segment in detail, incorporating tables and formulas to elucidate cost factors and trends.

Upstream Raw Materials: Supply and Cost Dynamics

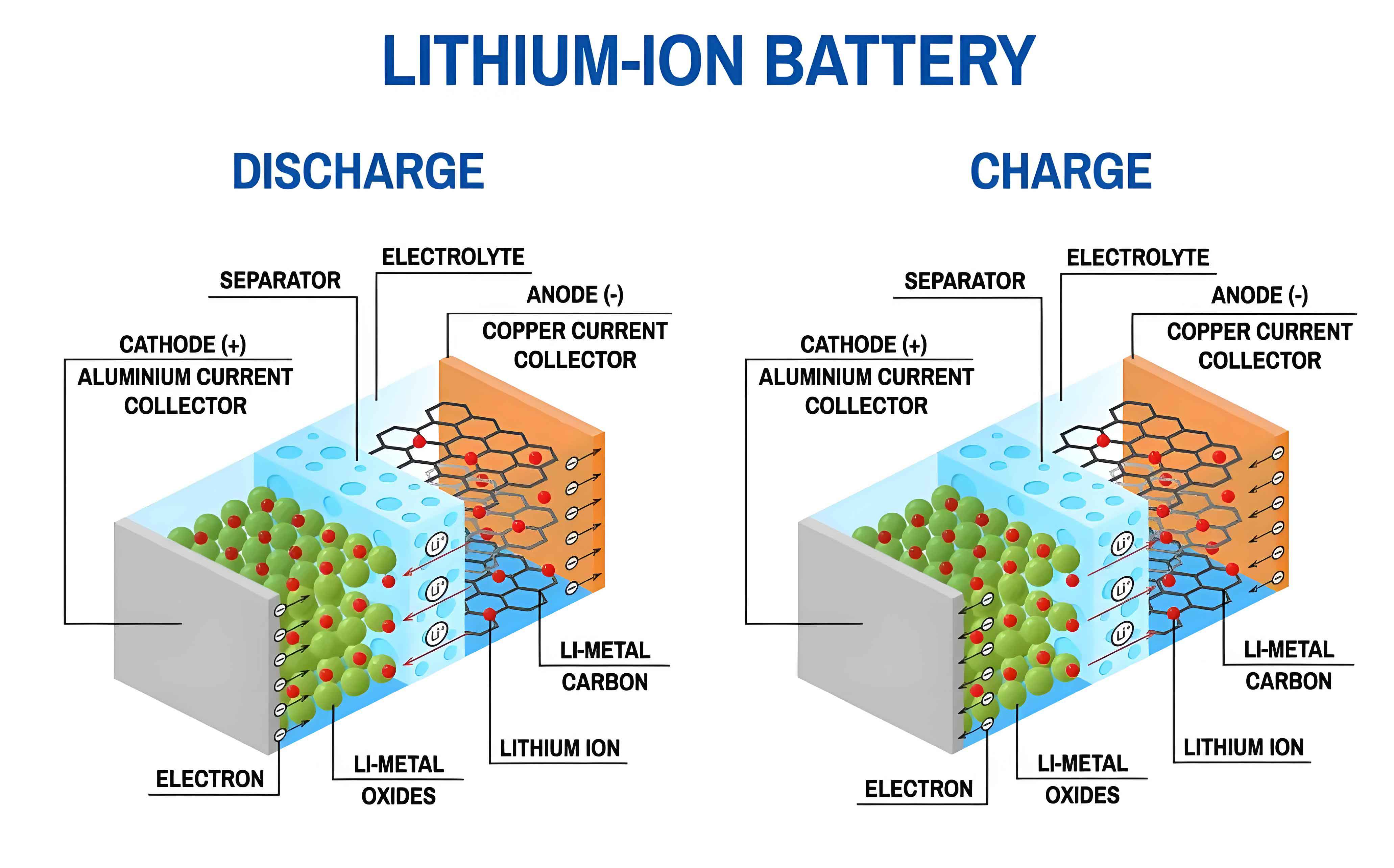

The upstream segment of the lithium-ion battery industry involves critical raw materials such as cathode materials, anode materials, electrolytes, and separators. From my research, the availability and pricing of these materials significantly impact the overall cost of lithium-ion batteries. For instance, cathode materials like lithium cobalt oxide (LCO), lithium nickel manganese cobalt oxide (NMC), and lithium iron phosphate (LFP) rely on metals such as lithium, cobalt, nickel, and manganese. The volatility in prices of these metals, due to geopolitical factors and supply chain disruptions, can lead to cost fluctuations in lithium-ion battery production. Anode materials, primarily graphite, also contribute to costs, while electrolytes and separators involve specialized chemical processes. I have compiled a table summarizing key raw materials and their roles in lithium-ion batteries:

| Component | Key Materials | Cost Influence |

|---|---|---|

| Cathode | LCO, NMC, LFP, lithium nickel cobalt aluminum oxide (NCA) | High, dependent on lithium, cobalt, nickel prices |

| Anode | Graphite, silicon-based materials | Moderate, graphite prices relatively stable |

| Electrolyte | Lithium salts (e.g., LiPF6), organic solvents | Significant, purity and stability affect performance |

| Separator | Polyolefin membranes (PP, PE) | Moderate, technological advancements reducing costs |

| Other | Conductive agents, copper foil, aluminum foil | Minor but cumulative impact |

To quantify cost variations, I often use a formula for raw material cost estimation in lithium-ion batteries. Let \( C_{raw} \) represent the total raw material cost per kilowatt-hour (kWh), which can be expressed as:

$$ C_{raw} = \sum_{i=1}^{n} (P_i \times Q_i) $$

where \( P_i \) is the price of material \( i \) and \( Q_i \) is the quantity required per kWh. For example, if the price of lithium carbonate fluctuates, the cost of lithium-ion batteries may shift accordingly. From my analysis, in 2022-2023, raw material prices for lithium-ion batteries experienced high volatility, with lithium prices peaking before declining due to factors like slowed demand growth and increased production capacity. This underscores the sensitivity of lithium-ion battery costs to upstream market dynamics. I believe that diversifying material sources and investing in alternative chemistries, such as sodium-ion batteries, could mitigate these risks for the lithium-ion battery industry.

Midstream Manufacturing: Production Processes and Cost Breakdown

The midstream segment encompasses the manufacturing of lithium-ion batteries, involving steps like electrode preparation, cell assembly, electrolyte filling, sealing, and testing. From my visits to production facilities, I have noted that automation and scale economies play crucial roles in cost reduction. The manufacturing cost \( C_{man} \) for a lithium-ion battery can be modeled as:

$$ C_{man} = C_{labor} + C_{equipment} + C_{energy} + C_{QC} $$

where \( C_{labor} \) is direct labor cost, \( C_{equipment} \) includes depreciation and maintenance, \( C_{energy} \) is energy consumption, and \( C_{QC} \) is quality control and testing expenses. With technological advancements, \( C_{labor} \) and \( C_{energy} \) have decreased as a percentage of total cost, while \( C_{equipment} \) remains significant due to high initial investments. For instance, the adoption of dry electrode coating and cell-to-pack (CTP) designs has streamlined production, lowering costs for lithium-ion batteries. I estimate that manufacturing costs for lithium-ion batteries have fallen by over 80% in the past decade, driven by innovations and mass production. However, challenges like ensuring safety standards and minimizing defects persist, impacting the overall economics of lithium-ion battery manufacturing.

To illustrate the cost breakdown, consider the following table based on industry data for a typical lithium-ion battery pack:

| Cost Component | Percentage of Total Cost | Trend |

|---|---|---|

| Raw Materials | 60-70% | Fluctuating with metal prices |

| Manufacturing Labor | 5-10% | Decreasing due to automation |

| Equipment Depreciation | 10-15% | Stable with scale |

| Energy and Utilities | 5-8% | Rising but offset by efficiency gains |

| Quality Control | 3-5% | Increasing with safety regulations |

This table highlights the dominance of raw materials in lithium-ion battery costs, emphasizing the need for supply chain resilience. From my perspective, continued innovation in manufacturing techniques, such as solid-state battery production, could further reduce costs and enhance the competitiveness of lithium-ion batteries.

Downstream Applications and Supply Chain Costs

The downstream segment of the lithium-ion battery industry includes applications in electric vehicles, consumer electronics, energy storage systems, and more. I have observed that the electric vehicle sector is the largest driver of demand for lithium-ion batteries, with global EV sales projected to exceed 20 million units by 2030. This growth fuels the need for high-performance lithium-ion batteries with longer lifespans and faster charging capabilities. Additionally, energy storage systems are becoming a key market, as lithium-ion batteries help integrate renewable sources like solar and wind into the grid. The supply chain costs here involve logistics, warehousing, and distribution, which add to the final price of lithium-ion batteries. A formula for total supply chain cost \( C_{SC} \) can be expressed as:

$$ C_{SC} = C_{procurement} + C_{production} + C_{logistics} + C_{inventory} $$

where \( C_{procurement} \) is raw material sourcing, \( C_{production} \) is manufacturing, \( C_{logistics} \) covers transportation and storage, and \( C_{inventory} \) accounts for holding costs. Optimizing this chain is vital for the lithium-ion battery industry to maintain affordability. For example, localized production hubs near EV assembly plants can reduce \( C_{logistics} \), benefiting the overall cost structure of lithium-ion batteries. I anticipate that as downstream markets expand, economies of scale will further lower costs, making lithium-ion batteries more accessible for diverse applications.

Battery Recycling: Emerging Supply Source and Cost Analysis

The recycling of lithium-ion batteries is an emerging sector that addresses sustainability and resource scarcity. From my analysis, recycling can provide secondary raw materials, reducing dependency on mining and lowering environmental impact. There are two main approaches: direct recycling for material recovery and second-life applications for reused batteries. The cost of recycling lithium-ion batteries, \( C_{recycle} \), involves expenses for collection, disassembly, chemical processing, and environmental management. It can be modeled as:

$$ C_{recycle} = C_{collection} + C_{processing} + C_{environmental} + C_{residue} $$

where \( C_{processing} \) includes hydrometallurgical or pyrometallurgical methods. I have found that recycling lithium-ion batteries is becoming economically viable, with unit margins improving as technologies advance. The global market for lithium-ion battery recycling is expected to grow significantly, driven by regulatory pressures and corporate sustainability goals. For instance, policies in the EU and China mandate recycling targets, incentivizing investment in this area. A table comparing recycling methods for lithium-ion batteries is provided below:

| Recycling Method | Process Description | Cost per Ton | Material Recovery Rate |

|---|---|---|---|

| Hydrometallurgical | Chemical leaching to extract metals | $3,000 – $5,000 | High for lithium, cobalt |

| Pyrometallurgical | High-temperature smelting | $2,000 – $4,000 | Moderate, focuses on metals |

| Direct Recycling | Physical separation and refurbishment | $1,500 – $3,000 | Variable, preserves structure |

This table illustrates the trade-offs in recycling lithium-ion batteries. From my viewpoint, enhancing recycling efficiency is crucial for creating a circular economy in the lithium-ion battery industry, mitigating raw material risks and reducing costs over the long term.

Market Analysis: Demand, Competition, and Price Trends

The global market for lithium-ion batteries is characterized by robust demand, intense competition, and evolving price trends. Based on my research, demand for lithium-ion batteries is primarily fueled by the electric vehicle revolution and the expansion of renewable energy storage. I project that global lithium-ion battery shipments could surpass 2,000 GWh by 2030, with China leading in production and consumption. The competitive landscape is dominated by Asian players, including Chinese, Korean, and Japanese firms, which collectively hold over 80% of the market share for lithium-ion batteries. A formula for demand forecasting, \( D_t \), can be expressed as:

$$ D_t = D_0 \times (1 + g)^t + \epsilon_t $$

where \( D_0 \) is initial demand, \( g \) is the growth rate, \( t \) is time in years, and \( \epsilon_t \) represents external shocks like policy changes. For lithium-ion batteries, \( g \) has historically ranged from 20% to 40% annually, reflecting rapid adoption. Price trends for lithium-ion batteries are influenced by raw material costs, technological advancements, and market competition. I have observed that prices per kWh have declined from over $1,000 in 2010 to around $100-$150 in 2023, making lithium-ion batteries more competitive against traditional energy storage options. However, recent fluctuations in lithium and cobalt prices have caused temporary increases, highlighting the volatility in the lithium-ion battery market. The following table summarizes key market indicators for lithium-ion batteries:

| Market Indicator | 2023 Value | 2025 Projection | 2030 Outlook |

|---|---|---|---|

| Global Demand (GWh) | ~1,200 GWh | ~1,800 GWh | ~3,000 GWh |

| Average Price per kWh | $110 – $140 | $90 – $120 | $70 – $100 |

| EV Penetration Rate | 15-20% | 25-30% | 40-50% |

| ESS Market Share | 20% of total | 30% of total | 40% of total |

This table underscores the growth trajectory of the lithium-ion battery industry. From my analysis, competition is intensifying, with companies investing heavily in R&D to improve energy density and reduce costs for lithium-ion batteries. I believe that market consolidation will continue, as larger players leverage scale to dominate the lithium-ion battery supply chain.

Policy and Regulatory Environment

Government policies and regulations play a pivotal role in shaping the lithium-ion battery industry. From my review of global frameworks, initiatives like subsidies for electric vehicles, carbon emission targets, and recycling mandates directly impact the demand and production of lithium-ion batteries. For example, the U.S. Inflation Reduction Act provides tax credits for domestically produced lithium-ion batteries, encouraging local manufacturing. Similarly, the European Green Deal sets strict sustainability criteria for battery imports, affecting the lithium-ion battery trade. I have noted that environmental regulations are tightening, requiring lithium-ion battery producers to minimize carbon footprints and adopt eco-friendly practices. This regulatory pressure can increase compliance costs but also drive innovation in greener lithium-ion battery technologies. A formula for policy impact on cost, \( C_{policy} \), can be modeled as:

$$ C_{policy} = \alpha \times R + \beta \times S $$

where \( \alpha \) is the cost of regulatory compliance, \( R \) is the stringency of regulations, \( \beta \) is the benefit from subsidies, and \( S \) is the subsidy level. For lithium-ion batteries, \( \alpha \) may rise with new recycling laws, while \( \beta \) can offset costs through incentives. I anticipate that policies will increasingly focus on supply chain security for lithium-ion batteries, promoting regional production and reducing dependency on imports.

Future Trends and Technological Advancements

Looking ahead, the lithium-ion battery industry is poised for continued evolution, driven by technological breakthroughs and market forces. From my perspective, key trends include the development of solid-state lithium-ion batteries, which promise higher energy density and enhanced safety. Additionally, advancements in silicon-anode and lithium-sulfur chemistries could further improve the performance of lithium-ion batteries. I expect cost reductions to persist, with the levelized cost of storage (LCOS) for lithium-ion batteries declining due to economies of scale and process innovations. A formula for future cost projection, \( C_{future} \), can be derived as:

$$ C_{future} = C_{current} \times e^{-kt} + \Delta C_{tech} $$

where \( C_{current} \) is the present cost, \( k \) is the learning rate coefficient, \( t \) is time, and \( \Delta C_{tech} \) represents cost savings from new technologies. For lithium-ion batteries, the learning rate has been estimated at 15-20% per doubling of cumulative production, indicating sustained cost declines. Moreover, the integration of artificial intelligence in manufacturing and supply chain optimization will enhance the efficiency of lithium-ion battery production. I also foresee growth in second-life applications for used lithium-ion batteries, such as in stationary storage, creating new revenue streams. The table below outlines potential technological advancements in lithium-ion batteries:

| Technology | Expected Impact | Timeframe | Cost Implication |

|---|---|---|---|

| Solid-State Batteries | Higher energy density, safer | 2025-2030 | Initial premium, then reduction |

| Silicon-Anode Integration | Increased capacity | 2024-2027 | Moderate cost increase |

| Lithium-Sulfur Batteries | Lightweight, high theoretical density | 2030+ | Potential for lower costs |

| AI-Driven Manufacturing | Improved yield and efficiency | Ongoing | Reduces operational costs |

This table highlights the innovation pipeline for lithium-ion batteries. From my analysis, these advancements will solidify the position of lithium-ion batteries as a leading energy storage solution, enabling broader adoption in transportation and grid applications.

Conclusion

In conclusion, the lithium-ion battery industry stands at the forefront of the global energy transition, with its cost structures and market dynamics shaped by raw material availability, manufacturing efficiencies, and policy frameworks. From my comprehensive analysis, I have highlighted the critical role of upstream materials, the cost-saving potential of midstream innovations, and the expanding downstream markets for lithium-ion batteries. The recycling sector adds a layer of sustainability, while competitive forces and technological trends drive continuous improvement. Despite challenges like price volatility and regulatory hurdles, the future of the lithium-ion battery industry appears bright, with projections indicating sustained growth in demand and further cost reductions. As we move towards a low-carbon economy, lithium-ion batteries will remain indispensable, powering everything from electric vehicles to smart grids. I am confident that ongoing research and collaboration across the lithium-ion battery value chain will unlock new possibilities, ensuring that this technology continues to evolve and meet the world’s energy needs efficiently and sustainably.